The problem with most incentive systems

Cash incentives play a much greater role in shaping organizational performance than most of us would like to admit.

When they are correctly designed, incentive plans stimulate employees to invest wisely, to use assets efficiently, to develop and exploit new opportunities, and to to improve performance.

Most incentive programs usually fail for the following reasons.

-

Setting the bonus on measures that send the wrong signals. Should bonuses be determined by sales, earnings, cash flow, rate of return, margins or market share, to name just a few of the measurement candidates? Choose the wrong measures and people will do the wrong things as surely as night follows day.

-

Managers and employees are unable to respond to the bonus incentives because they lack requisite business basics and financial know-how. Many of them simply cannot connect their day-to-day actions and strategic decisions to the outcomes that will be rewarded by their bonus or share option. Companies have not properly communicated how their incentive plans work, and managers and employees lack the training they need in business literacy, and in accounting and financial management, in order to respond appropriately.

-

The most common mistake in this area is basing bonuses on meeting or exceeding the annual budget. Linking bonuses to the budget only encourages managers to set conservative, easy-to-achieve goals.

-

Designing incentive plans in a vacuum and then sealing them off from the on-going managing processes. Planning, finance, investor relation and human resource departments each pull in separate directions, with their own agendas, measures, champions and constituencies. Their unwillingness or inability to coordinate and speak a common language confounds the seamless integration of incentive programs into business management. The measures used to determine bonuses, for instance, are often not clearly highlighted, or, in some cases, even computed, on regular management reports and scorecards, or in the planning, capital budgeting, and decision-making procedures. Operating managers find it difficult to respond to incentive plans when they are tugged in so many directions, and when they cannot easily discern which decisions and which strategies will directly contribute to their personal incentive reward.

-

Incentives are often excessively dependent on short-term performance. Bonuses depend so heavily on the results generated within one year that managers do not pay sufficient attention to long-term issues, and do not invest enough in projects that will increase their capabilities to succeed over a longer horizon. Managers are also tempted to manipulate accounting to produce results they cannot sustain over the longer term. The recent experiences of Lucent, Enron and Tyco are testimony to the power of short term incentives to destroy long-run value.

-

Over reliance on options. Options do align managers with the shareholders, but only in the most abstract way. Outside the very top ranks most managers cannot fathom how their decisions directly affect the share price, particularly in large complex companies. Options also are far more expensive than they appear. Although accountants do not record a charge to earnings from issuing options, the smart investors who set share prices look ahead and discount for the cost to retire share issued through the options program.

-

Concentrating incentives among top managers instead of involving all employees, and offering incentives insufficiently large to encourage people to make unpleasant decisions. In most companies the board wants to limit the cost of making incentive payments. But that need not be the case.

If bonuses are structured as a share of performance improvements–as a set percent of the additional wealth that is created by the ingenuity and energy of the employees, then the potential bonus awards can legitimately be quite large, indeed, uncapped, for all employees. With such a bonus structure bigger bonuses are better for all concerned.

There is no question that such bonuses – even quite large ones – can be financed, because they are automatically self-funding. They are paid for out of the extra efficiency and growth that stems from giving the people a piece of the action. Bonus payments of this type are certainly not a cost to be minimized but are rather a share of the value to be maximized. After adopting such an “ownership-oriented” incentive philosophy, a board of directors should no longer feel obliged to limit potential bonus payments, and no longer should they be reluctant to extend a bonus program to even the lowliest worker.

You need to create an ownership structure

Give employees a stake in the success of their business, and the business becomes more successful. Make the employees into owners, and the real owners can relax. Nothing could be more important for good corporate “governance” than getting managers and employees to think and act like owners by paying them like owners.

Many companies attempt to foster an ownership spirit by arranging for employees to hold company share or options. While they differ in the details, share and options both give managers and employee’s incentives to think and act like owners, because they reward them like owners. However, all forms of share-based incentives have significant disadvantages. Many companies are finding that as they grow larger and more complex, for example, share and option grants lose much of their effectiveness, particularly outside the top executive ranks.

The first problem with these equity plans is that there is only one overall share price for a company, but a large company is usually composed of many distinct business units and activities. Share options have little power to motivate the right kinds of behaviours outside of their top executive teams. Any one person, even someone fairly senior, has so little influence on overall performance that he or she will be tempted to say, if only under their breath, “I hope everyone else is working hard to get the share price up, but I might as well go play golf.” In economics that predictable behaviour has long been known as the “free rider” problem. It occurs when everyone wants to jump on a wagon to go for a ride, but no one has the incentive to be the one pushing. It is also happens when an ambitious soul wants to push a wagon fast but finds he can not budge it for the weight of all the loafers on board.

The “top guns” want to see a more direct link between their pay and their performance. They want to be measured and rewarded more on their efforts rather than diluted with the conflicting inputs from so many other people and divisions. They want ownership in what they can control or influence.

Put another way, share and share options are like issuing only one report card for a whole class of students, just as there is only one share price for a whole company of people. The best students (or employees) are demoralized, and the worst ones thrilled to coast on everyone else’s efforts. For ownership incentives to work, a company must be broken down into smaller units, and employees must feel that they have an ownership interest in the business unit or activity with which they are directly involved.

Another shortcoming of share options is that corporate managers and employees are often perplexed about the performance factors that drive their share price. Many of them incorrectly believe that accounting measures of earnings or cash flow (such as EBITDA) drive the movements in their company’s share price. But as will be explained later, the best internal measure of how well a company is performing and how its share price will respond is the firm’s economic profit. Even with options in hand, managers may aim at the wrong financial targets or apply flawed criteria to make decisions. In this respect issuing options gives managers an incentive to win a game in which they do not really understand how to score points.

A third problem is that a company’s share price cannot outpace the overall share market indexes indefinitely. At some point investors will fully anticipate (if not exaggerate) the firm’s prospects for future growth. The company’s share performance will plateau even as its profits continue to spiral upwards. Once that happens it becomes difficult for a company to entice new hires with options.

Despite their shortcomings, share options should almost certainly be a part of the overall compensation mix, particularly for the top team that is more financially literate and responsible for overall results than middle managers or the rank and file. In general, however, a better way to foster a pervasive ownership culture is to limit share option grants and replace or supplement them with cash bonus plans that generously reward business unit and corporate performance. This strategy has many advantages compared to simply showering employees with options and hoping for the best.

Tying bonuses to business unit performance minimizes the incentive for managers and employees to free ride. They are held accountable to and rewarded for results that they influence directly. Tying a portion of the bonuses to company-wide results serves a complementary purpose. It preserves the incentive for teamwork and collaboration. Compared to the bluntness of corporate share ownership, bonus plans can be structured to target the appropriate balance between the competing aims of individual accountability and corporate-wide cooperation.

Bonus plans can also be far more concrete, understandable, and actionable than share ownership. They can be based on a select group of measures that are highly correlated to market value, but that are also far easier for managers and employees to understand and influence.

Bonus plans also can be tailored to provide performance incentives long after a company’s market value has levelled off. It is just a question of paying bonuses when the actual profits exceed the amount that investors expect and have factored into the company’s share price.

For this alternative strategy to succeed, the bonus plans must be carefully crafted to create incentives that are equivalents to having an ownership in a business unit and the overall company. They must offer the unlimited upside of an owner, but must also subject managers to risk if the results cannot be sustained over a strategic horizon. Most bonus plans fail to do that.

Use Economic Profits to Measure and Reward Performance

The first question to ask when designing a bonus plan that replicates the incentive of an owner is how to measure business performance. The right measure of corporate performance will have strong ties to the amount of additional wealth that a company produces for its shareholders and by extension for society at large. It will guide people to make the decisions that will generate the added value necessary to fund their bonus, to reward the shareholders and to reinvest in business growth.

The ideal measure also will be readily understandable by business people. It will clearly connect to their day to day decisions and to the levers that they can manipulate in the course of running their businesses, whether those levers are cost control and productivity, asset and supply chain management, marketing, customer satisfaction or growth.

Economic Profits (also called EVA by Stern Stewart) is the way to measure profit. In simplest terms, EProfits is a firm’s net operating profit after taxes, or NOPAT, less a charge for using all capital, equity as well as debt, as illustrated below.

|

Sales |

$100 |

|

Operating costs |

80 |

|

Operating profit before tax |

20 |

|

Tax at 40% |

8 |

|

NOPAT |

$ 12 |

|

Loans |

$ 40 |

|

Shareholders’ equity |

80 |

|

Capital |

$120 |

|

x The cost of capital |

10% |

|

Capital Charge |

$ 12 |

|

EProfits |

$ 0 |

Capital represents the sum of all funds a company has raised from its investors or retained from its earnings. The sample company has raised a capital total of $120 from its lenders and shareholders. Companies use their capital to purchase the business assets they need for operations. Every time a company buys an asset, it must raise more capital from its investors. If managers are able to use assets more effectively, they will require less capital, and that surplus cash can be returned to investors to invest in other companies and fuel more growth elsewhere in the economy. Allocating and using capital wisely is thus a key to economic success. By charging managers for using capital, EProfits directly encourages managers to use capital and assets efficiently and effectively.

The capital charge is determined by multiplying the amount of capital by the cost of capital. The 10% cost used in the example is not a cash cost the company must pay. It is an opportunity cost. It is equal to the rate of return that the lenders and shareholders could have earned by investing their funds in a collection of shares and bonds that have the same risk profile as investing in the company. To measure it, start with the rate of interest on government bonds. For illustration, assume that the government bond rate is 6.0%.

Investors in an individual company will expect to earn a return over and above the government rate. They will demand additional compensation for bearing the risk in the company’s business. A company’s profit outlook can shift due to competitor moves, price changes, demand shifts, a downturn in the economy, or any of countless factors that cannot be predicted in advance. As a result, the bonds and shares issued by individual companies fluctuate in value far more than do government bonds. Investors do not like that risk because they may be forced to sell when the value of their investments is low. Investors will be willing to take the risk only if they can expect to earn a return on their investments that generally ranges from 2% to 10% more than the government bond rate. That risk premium will vary by the company, its industry sector, and the mix of capital it employs between loans and shareholder funds. In the example a 4% risk premium was used for illustration. The 10% cost of capital is simply the 4% risk premium plus the 6% government bond rate.

The table indicates that the sample company is earning a NOPAT profit that is just large enough to cover the capital charge. The company is giving its investors as good a return on their investment as they could earn elsewhere while taking the same degree of risk. Even though the company is making $12 in actual NOPAT profit it is only breaking even in true economic terms. It is earning just the profit it needs to pay interest to its lenders and to give the shareholders the return they expect through a combination of dividends and an increase in the value of their share. That result is not bad, but it is not good either. It is breaking even.

Increasing EProfits is not the same as increasing reported accounting earnings. It is an entirely different challenge and can lead to dramatically different decisions. Companies can quite easily manufacture growth in their accounting earnings and earnings per share simply by pouring tons of capital into their business.

The preoccupation with earnings growth is so deeply rooted among corporate managers that it warrants understanding its flaws in more detail. Any company’s earnings growth is the result of multiplying together two contrasting factors. The first is the rate of return that the company earns on its new investments. That measures the quality of the company’s investments. The second factor is the investment-spending rate, a measure of the quantity of the company’s investments. The problem with looking at earnings growth alone is that quantity of investment can always make up for a lack of quality.

Growth = Rate of Return x Investment Rate

To be more specific, the rate of return tells how much a company’s profit increases for every additional dollar of capital it employs. A company that earns a 20% rate of return, for example, increases its profit by 20 cents for every dollar of additional investment it makes. However it is achieved, earning a high return is a key indicator of overall operating efficiency.

The other factor that drives growth is a quantitative measure of investment intensity. A company’s investment rate is the ratio of how much money a company is investing to the amount it is earning as profit over the same period. If a company invests $80 in new business assets and earns $100 in profit over that same period then its investment rate is 80%. A company with an investment rate less than 100% has a positive “free” cash flow. It invests less than it earns and so has excess cash to distribute to its investors. A company with an investment rate over 100% has a negative free cash flow. It is forced to raise capital from external sources to supplement its retained earnings, such as through new bank borrowings, bond issuances, or new share offerings.

Consider how the formula applies to two hypothetical companies that are both growing their earnings at 10%. If they were the same in every other way one would be forced to conclude that both firms have the same value. But if Company A earns a 15% rate of return and Company B only a 5% return, then A must be more valuable even though it exactly matches B’s earnings growth rate:

Growth = Rate of Return x Investment Rate

A. 10% = 15% x 66.7%

B. 10% = 5% x 200.0%

Company A is more valuable because it needs to invest only a fraction of its earnings to grow whereas B must invest twice its earnings. By earning a higher rate of return A is better able to finance growth from internally generated funds. It can generate a positive free cash flow to reward its investors while Company B must constantly raise more cash from them. Company B is simply manufacturing growth by making a lot of bad investments. The simple example points up an important business lesson: Earning a high return on capital is far more important than achieving rapid earnings growth. Acquisitions that increase a company’s growth but produce a low return will penalize the acquirer’s share price and reduce its shareholder value. This being the case, it is unfortunate that so many companies today still tie incentive pay to growth in earnings or earnings-per-share.

EProfits directly incorporates this business maxim. If management pours capital into projects that produce returns less than the overall cost of capital, EProfits will sink as accounting profits surge. Consider our first example company once again. Assume that management sets and achieves a goal to double sales and earnings, but by doing so it must more than double the amount of capital committed to the business. Let’s assume capital balloons from $120 to $300 in order to fuel the growth.

|

Sales |

$100 |

$200 |

|

Operating costs |

80 |

160 |

|

Operating profit before tax |

20 |

40 |

|

Tax at 40% |

8 |

16 |

|

NOPAT |

$ 12 |

$ 24 |

|

Loans |

$ 40 |

$100 |

|

Shareholders’ equity |

80 |

200 |

|

Capital |

$120 |

$300 |

|

x The cost of capital |

10% |

10% |

|

Capital Charge |

$ 12 |

$ 30 |

|

EProfits |

$ 0 |

$ - 6 |

|

NOPAT less the Capital Charge) |

|

|

The accounting vital signs look robust–sales and earnings in the right hand column are double their former levels–but in fact the company is much weaker. EProfits erodes from breakeven to a $6 loss. The EProfits loss is due to earning a rate of return lower than the cost of capital. Notice that the additional capital investment of $180 generates only a $12 increase in NOPAT. The ratio indicates that management is earning only a 6.7% rate of return on its investments when their investors could have earned 10% in the market.

Publicly listed companies that invest in low return projects reduce their price-to-earnings multiple. In fact, it is quite possible for them to reduce their P/E multiple so much that their share price shrinks even as their earnings expand. They become vulnerable to takeover and restructuring, and the top team is exposed to losing their jobs. Without facing such a hostile market discipline, private companies and government agencies can go on indefinitely destroying value by investing capital unwisely. Such enterprises are in even greater need of EProfits to send the rights signals to business leaders.

EProfits represents the single most reliable scorecard to weigh the value of a business or business decision. It is the measure that properly weighs and integrates all the pluses and minuses of a business decision into a decisive overall score. For instance, EProfits properly pits the benefit of producing greater customer satisfaction and generating more sales revenue against the total operating and capital costs of servicing the additional business.

EProfits measures all of the ways that performance can be improved and wealth can be created in any business. Put another way, anything that anyone can do to improve a business will show up as an improvement in EProfits. No other measure or combination of measures has that unique property. Consider that to increase EProfits, managers will want to do all things that will:

-

improve operating efficiency (by cutting costs and adding to profit without adding to capital);

-

enhance asset management (by reducing the investment in assets that earn less than the cost of the capital);

-

increase profitable growth (by making new investments that earn returns over the cost of capital); and

-

reduce the cost of capital (by implementing the most effective financial and investor relations strategies, and by increasing the transparency and account ability to the share market.

EProfits can offer even better guidance when performance distortions that arise from generally accepted accounting principles are eliminated. If EProfits was measured directly from reported accounting numbers, for instance, what manager would want to increase spending on a sound research project or on advertising to promote a promising new brand? According to standard accounting, those outlays must be immediately charged to profit, but the benefits are likely to materialize down the road. Which managers would want to take a charge to earnings following a restructuring of their business even if the restructuring was necessary and value adding? To overcome these obstacles, Stern Stewart has developed an alternative set of accounting rules that enable managers to measure their EProfits profit more accurately and better guide their decision-making. The rules are applied consistently and only for internal management reporting purposes.

One rule is that, instead of charging research and brand building outlays to earnings, they are added to a new balance sheet account for “intangible assets.” The intangible asset is written off as an earnings charge over the future time periods when the benefits from such spending are expected to increase profit. This one-two punch gives managers more freedom to increase or maintain intangible spending without fearing their bonuses will suffer in the short term, but at the same time holds them accountable for subsequently earning enough profit to cover the full cost of the intangible investments over the long term.

By following this practice, managers have more useful information on which to judge results and base decisions. Also, top managers often feel more comfortable delegating more decision authority as the new accounting makes people below them more accountable for their spending decisions. Nearly 100 such rules have been identified to eliminate distortions and positively influence behaviour. The rules vary quite a bit depending on the company and industry it is in. In practice companies usually apply only the five to fifteen most significant adjustments when they measure EProfits in their internal management reports. They wisely balance the trade-off between simplicity and precision.

EProfits also is important because it is the financial measure that directly determines the market value of every company. To be specific, EProfits is directly linked to another measure called MVA, or Market Value Added. MVA measures the difference between the share market value of a company and the amount of capital it has employed:

MVA = Total Market Value – Total Capital Employed

MVA is a vital measure of business performance because it represents how much wealth a company has created for its investors and for society. It shows the difference between how much cash has been put into the business and the cash out value of the business. It is like buying a home for $600,000 and selling it later on for $1 million. The cash you put in compared to the cash you get out indicates that you have increased your wealth by $400,000. Just as every person wants to maximize their wealth, every company should strive to increase its MVA as much as possible in order to enlarge the value of its investors’ savings.

Sophisticated investors use many different approaches to figure out how much they will pay to own a share in a company’s value. But all of those methods boil down to variations on a fundamental principle of market valuation, namely, that any company’s MVA is determined, in effect, by summing up the stream of EProfits profit that investors believe the company will earn and then discounting that stream to a present value:

MVA = the discounted present value of future EProfits

This relation works because EProfits subtracts the cost of capital. It sets aside the amount of profit that must be earned as a minimum in order to give investors the return they expect from their investment. As a result, if the market thinks a company’s EProfits will be zero, so that its investors will earn just the return they are seeking, then that company will just break even on its MVA, too. The market value of that company will just equal the book value of its capital, and its MVA will be zero.

Our sample company, you may recall, initially fell into that camp. It produced zero EProfits, and that made it worth zero MVA. Its market value would be equal to the $120 book value of its capital. The firm could continue to invest capital and buy more assets, and increase its sales, earnings, size, and maybe even its market share, but if it persisted in earning no EProfits its market value would increase only as much as the additional capital it employed. It would preserve, but not enhance or diminish, the wealth of its investors. It would break even all around.

Worse things could happen. If the company reduced its EProfits it would only succeed in reducing its MVA. Recall the case in which a $180 investment intended to double the sample company’s sales and earnings ended up reducing its EProfits by $6. The only way investors could earn the return they want when the company isn’t earning it for them would be for them to buy into the company at a market price that discounts the value of the capital employed in the business. To be precise, the investors will subtract the present value of the EProfits loss from the company’s market value. In the case at hand the firm’s MVA is reduced by $60, the result of capitalizing the annual $6 EProfits loss at a 10% cost of capital. That means that the $180 investment would only add $120 to the company’s market value; the other $60 in value would be obliterated, and the loss would be spread over all the shareholders. Growth, even rapid growth, is simply not a guarantee of business success.

The link of EProfits to MVA is extremely important for business managers. It means they can use EProfits to evaluate all new projects or investments. They can determine the value of pursing new products, plants or markets, for instance, by projecting and discounting the EProfits they believe the new investments will produce. They should take the initiatives that will add the most to MVA and shun the rest. Projecting and discounting EProfits will always give the same net present value (NPV) answer as projecting and discounting cash flow. But using EProfits is better because it can also be used to measure performance and determine bonuses after the investment has been made, but cash flow cannot. EProfits is simply a better way to get managers truly to rely upon NPV thinking rather than just giving it lip service.

EProfits is an ideal measure for determining bonuses. EProfits directly connects business decisions to the mission to create wealth, and it sends all of the right signals to managers and employees in ways that are easy for them to comprehend and use. EProfits is also suitable for private firms and government agencies because it can be computed directly from their financial reports. For the same reason it is suitable to measure and reward the performance of individual business units within companies. EProfits can simulate the incentives of ownership even when a share price is unavailable. Also, because a company and its owners are always better off with more EProfits than less, the bigger the bonus, the better it is for all concerned.

Using EProfits® to Create A Phantom Equity Bonus Plan

Bonus plans can be structured in many ways, but most of them don’t work very well. Indeed, poorly designed plans actually inhibit sound decision-making and reduce wealth. To make employees truly think and act like owners, they must be paid like owners by using a bonus plan that has special characteristics. The plan must always be tailored to an individual company, of course. Organization structure, risk tolerance, business strategy and culture are just some of the factors that ought to influence the design of the bonus plan.

There are nine principles that transcend those specifics and provide general guidance for designing incentive plans that work.

Alignment.

The incentive payments that managers and employees receive must be strongly linked to their success at creating shareowner wealth. It has already been shown that EProfits provides the right measure for this purpose. Recall that EProfits measures profit after subtracting the cost of capital and eliminating accounting distortions that make it difficult for managers to understand the economic reality of their business. EProfits automatically makes employees accountable for investing and using assets wisely. It shines a bright light on the four ways any manager can take to improve its performance and create wealth, namely, by increasing operating efficiency, improving asset management, pursuing profitable growth, and implementing the best financial strategies. It is an ideal measure to use in structuring incentive plans that motivate people to think and act like owners.

Improvement.

The bonuses should not be paid from EProfits, but from the increase in EProfits. Taking a troubled business with a negative EProfits and making its EProfits less negative is as valid a way to improve performance and create wealth as taking a star performer with a positive EProfits and making it even more positive. Paying for EProfits improvement levels the playing field. Talented managers and employees can be just as motivated to join tough businesses that need to be turned around and restructured as to join the best businesses. Fixing problems can be as lucrative as capitalizing on opportunities. Lou Gerstner’s impressive reversal of IBM’s fortunes is one good example.

Concentration.

The bonus pool should be funded as much as possible by one overall measure of total business performance rather than a group of measures, particularly for the top team. Concentrating on a single measure keeps the incentive simple and easy to communicate. It also curtails parochial behavior. Many companies judge managers in production by one set of measures and those in sales and marketing by others. The top team may be paid on still another set. Each group is motivated only to see their point of view and to work against each other. But by uniting all their incentives on improving a common measure, more cooperation across functions and organization levels is forged. With everyone accountable for contributing to value, there is nowhere to hide.

For all of its advantages, many corporate executives are reluctant to concentrate incentives on one metric. Many of them do not truly understand EProfits and how it implicitly incorporates the totality of business performance. Still others are unwilling to invest in the training their employees would need to understand EProfits and how to influence it. These executives prefer to consider a long list of measures in their bonus plans. They count on those measures to communicate their strategy and educate their people, instead of using training and leadership for those purposes. They should reconsider the cost of providing better training and more effective communication against the cost of a complex, and ineffectual, bonus plan.

Other managers like to use many incentive measures as a way to convey that many factors are important to achieving overall business success. But in their attempt to clarify, these business leaders often end up confusing their people and diluting their accountability. I once encountered a company that put a 10% weight on 10 separate measures in their bonus plan. In their attempt to make many things important they had made nothing seem important. Their approach was like judging a basketball team by tracking various statistics, such as blocked shots, rebounds, assists, field goal percentage, free throws, penalties, and so forth, then combining them into a score by assigning various weights and summing up. But victory is not determined by an arbitrary addition of statistics. The score of the game is what indicates victory, and in business EProfits measures the score.

Another reason top executives often want a measurement array is to gauge and reward individual performance. But they are expecting the bonus plan to do too much. They should consider the GE approach: grade individual performance through a disciplined, documented, personal review process, and mete out rewards through merit increases, promotions, and share option allocations. Count on the bonus plan solely to motivate value centric thinking by sharing the value added. This approach avoids diluting the simplicity and purpose of the incentive plan.

To the extent top management simply insists on using the bonus plan to recognize individual performance, EProfits should still be used to determine the overall size of the bonus pool, with the bonus pool allocated (at least in part) according to assessments of personal or departmental performance. Then if there is no EProfits there is no bonus, regardless of an individual’s performance. As a consequence, each employee has the incentive to cooperate, and business leaders have the incentive to develop personal and departmental objectives that contribute to the overall EProfits performance.

Concentrating incentive pay on EProfits does have a downside, however. As was noted, managers and employees need to be thoroughly trained to understand EProfits and how to use it in making decisions. They also need access to frequent “scorecard” reports that trace the EProfits results to the individual factors and measures that they can directly influence. But these are things that well-managed companies should be doing anyway.

Materiality.

The potential bonus must be large enough to motivate people to work hard and make valuable decisions that are unpleasant. They must be so attracted by the prospect of earning a big bonus that they are willing to put economic considerations above internal politics. Once again, EProfits is ideally suited for this purpose because it amplifies corporate performance improvements into lucrative rewards.

To see how, consider a board that wants to establish an overall bonus pool of $1 to reward deserving employees. As shown in the table, management projects sales to be $100, and budgets operating costs (including taxes) of $80 and capital costs of $15. The plan calls for $20 in NOPAT profit and $5 in EProfits. Also assume that management intends to grow its business and EProfits by 20 percent or by $1 year over year.

|

Sales |

$100 |

1% |

|

Costs, including taxes |

80 |

|

|

NOPAT |

20 |

5% |

|

Capital |

150 |

|

|

x The Cost of Capital |

10% |

|

|

Capital Charge |

15 |

|

|

EProfits |

5 |

20% |

|

Increase in EProfits |

1 |

100% |

|

(at a 20 % growth rate) |

|

|

The right hand column indicates that anything from one percent of sales, five percent of profit, 20 percent of EProfits or 100 percent of the increase in EProfits will produce a $1 bonus pool if the business plan is met. But which of the bonus plans is best? At the one extreme, applying a one percent weight to sales provides an insignificant incentive for employees to strive and exceed plan by generating more sales. Another problem is that employees have no incentive to manage any other aspect of the business. If they are motivated at all it will be to spend lavishly to spur as much sales growth as is possible, and the return be damned. The bonus incentive is weak and counterproductive.

By moving down the chart the bonus pool is established by applying progressively larger percentages to ever-smaller numbers. The bonus percentage is 5 percent of profit versus 1 percent of sales, for instance. Offering employees a bigger share of bottom line results is always better than offering them a smaller share of top-line results. For one thing, the employees become more accountable for the totality of the business. They still have to worry about satisfying customers and driving top line revenues, but they must also control costs and manage capital.

Another reason to prefer bottom line incentives is that the incentive is amplified. Employees will have a far more substantial opportunity to make a lot of money if they can significantly improve overall performance. The 20 percent weight on EProfits, for instance, is four times the 5 percent weight on profit and twenty times the 1 percent weight on sales. Even small improvements in EProfits translate into consequential rewards. Taking this principle even further, the best bonus plans are those based upon sharing the increase in EProfits. It offers the most leveraged incentive for managing all aspects of the business, including growing the business profitably.

Unlimited Upside.

Many companies limit the size of the bonus they will pay. The most common ceiling is 1.5 times a target bonus. That is understandable, perhaps even necessary, when the bonus is based on measures that are only loosely linked to creating wealth. But there is no need to limit a bonus based on increasing EProfits because more EProfits produces more wealth. Limiting the bonus opportunity only discourages employees from taking actions that can create additional wealth, and encourages them to slow down and build reserves in good times rather than stretching for all the profit the business is capable of producing. To make managers think like owners’ they need to be paid like owners—with no limit on their upside potential.

Precautions are necessary, however. The bonus requires checks and balances. The board of directors must be sure that the EProfits gained in one year can be maintained in future years. Managers must be discouraged from boosting short-term profit in ways that diminish long-term vitality.

Sustainability.

One effective mechanism is to hold back part of large bonuses, and then to pay them out over time only if the new, higher level of EProfits is maintained. If EProfits slips, the deferred bonus would be canceled in the same way that share prices tumble when a company’s performance deteriorates. “Banking” exceptionally large bonuses and subjecting them to cancellation encourages employees to make decisions in the long-term interest of the company, and to carefully balance risks against potential rewards.

Retention.

If a manager or employee leaves, the bonuses deferred from prior years are forfeited. The departing people surrender the equity they have built up in their bonus bank as a penalty for taking their accumulated experience elsewhere. Good performers have a strong incentive to stay put and build up more equity in the firm.

Definitive.

There should be an explicit, objective and reliable link between the bonus and performance. Employees should not have to guess at how they will be judged, and they should clearly understand the reward they will receive as they improve EProfits performance. One good approach is simply to develop a formula such that the bonus is a stated percent of the current and cumulative improvement in EProfits. The percent of EProfits used in the formula should be set in advance, ideally for a minimum commitment of three to five years, and the sharing rate should not vary as business plans and performance shift with the passage of time. Managers and employees should be furnished with tools that enable them to project the EProfits outcomes of alternative decisions and to understand the bonus they will be entitled to receive if they are successful with their plans. That encourages them to think and act like owners because they can anticipate earning the return of an owner.

It is tempting to tie the bonus to achieving budget and planning targets as those are revised each year. After all, why not pay managers and employees to achieve the plans that they are charged with executing? In practice, however, that is extremely counterproductive. Managers quickly realize that the best way to earn a big bonus is to downplay the real opportunities in their business and to withhold valuable information from the headquarters staff. Planning invariably bogs down into adversarial negotiations.

With a definitive bonus plan, managers become more ambitious in setting goals and more willing to change their strategies as circumstances dictate because they are rewarded not for beating their plan, but for whatever EProfits their planning has helped them to achieve. Internal collaboration also is enhanced. Field managers and corporate staff want to partner to find and implement the strategies that will produce the most EProfits, since that is what their pay is based upon. Breaking the link between bonuses and budgets is a key to liberate budgeting and planning, and to make them more flexible, more strategic and more interactive.

Participation.

Ideally, everyone—from board members to general managers to the lowliest employees—should participate in an EProfits bonus plan. The underlying bonus plan structures should be similar from top to bottom to unite them all in a common quest for genuine business improvement and wealth creation. It also is a good idea for people to participate in the bonus plan for their own division and for closely related units as well as for the total company. Overlapping their incentives motivates people to cooperate, share best practices, and take on challenges for the good of the whole.

Taking all elements together, EProfits bonus plans can help instill an ownership culture by giving managers and employees an incentive that is equivalent to that of a shareholder. Carefully designing and calibrating the bonus plans, and explaining the program in a clear and convincing manner are critical success factors. Weaving EProfits throughout a company’s reporting and planning processes is also vital. So is extensive education in using the new EProfits decision tools, and in relating EProfits to the measures that appear on the company’s balanced scorecard.

Integrating EProfits and Incentives into a Total Management System

Incentive plans based on EProfits cannot be designed and implemented in a vacuum. They should be seamlessly integrated into the entire array of management processes. Bonus plans and share option programs also ought to culminate in total pay packages that properly balance risk, cost and incentive. EProfits itself should become the glue that binds together and informs all aspects of management and strategic thinking. It should be the focal point for management reporting, for decision-making and planning, for incentives, and for communicating with employees and investors. Only then can management expect to reap the full benefits from using EProfits, and only then will the incentive program be simple and truly effective in influencing how managers and employees actually behave.

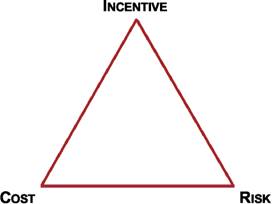

Consider a company that is about to introduce incentive pay for the first time. If the share options and bonus plans are added on top of existing wages, they are apt to introduce an unacceptably high cost to the shareholders. After all, shareholders are paid only after all the incentive fruits are shared out to managers and employees. If the incentive payments fully offset base pay, managers and employees will not be adequately compensated for the additional risk they are asked to bear. A key question is how to introduce incentives at a reasonable cost to shareholders and without imposing an uncompensated risk on employees. The trade off among cost, risk, and incentive is represented by the triangle below.

The left to right trade off between cost and risk could be addressed simply by paying the wage that would keep employees happy in their current role. By doing so a company will never run the risk of paying them too much or too little. But such a strategy provides no incentive. Only by introducing a variable payment based on performance will people have an incentive to care about performance and shareholder value. Compensating employees for taking on some of the risk of a shareholder is an unavoidable cost to introducing a shareholder-oriented incentive plan, but having the right kind of incentive plan can minimize that cost. An incentive based upon EProfits is capable of achieving the greatest incentive at least cost because it most closely aligns the decisions and incentives of the insiders with the results achieved for the shareholders.

Even with an EProfits plan, however, a company must still increase the total compensation that employees can expect to receive to compensate them for bearing more risk. This is illustrated in below.

At the far left, compensation is entirely in the form of debt-like wages and other fixed benefits, including super contributions. Moving to the right, the compensation mix shifts to introduce pay that is more at risk based on performance, such as by introducing an EProfits bonus and a share option plan. Increasing the risk based on the company’s performance is necessary to motivate the right behaviours, but it also requires an increase in the value of the total compensation that employees can expect to receive for delivering the results that investors expect.

Share options should also be a part of the incentive compensation mix, particularly for the senior people who have a direct influence on overall strategy and results. There are three types of option plans to consider.

-

The most typical is the fixed value grant. In this plan the number of options granted each year is adjusted up or down in order to maintain the same value. If the share price has gone up, so that each option is worth more, the employees are granted fewer new options. On the other hand, if the share price has gone down, the number of options granted increases. The objective is to give employees the same amount of compensation each year in the form of the value of the options they receive.

-

A very different approach is the fixed number grant. In this program the company announces that for a period of several years it will grant the same number of options regardless of the share performance over that time. If the share price goes up, the value of all options rises, not just those already in hand but also the ones that will be issued in the future years. Compared to the fixed value plan, this plan provides a more powerful incentive because share price gains translate into much bigger potential rewards. On the other hand, there are even bigger penalties if the share price falls because the entire package of options, including ones still to be granted, will decrease in value. The employees have a lot more at risk on the performance of the company over time compared to a fixed value grant program.

-

A third approach is an even riskier variant on the fixed number plan. Under an up-front grant program, the company immediately hands out all of the options that it would plan to issue over the next three to five years. There are no further option grants over the period, and the exercise price for all the options is set at the market price at the time of the grant. Managers and employees instantly feel a tremendous incentive to improve performance and value, making this the most powerful, but also the riskiest share option strategy. It provides incentives that resemble those found when managers participate in a leveraged buyout of their company.

If you want to provide people with more incentive, you must increase their risk. If you increase their risk, you must compensate them for bearing that risk or else they will look for a better deal. In the end the best option plan for a company will depend upon the risk preferences and financial sophistication of the managers. The most important consideration, however, is the underlying risk of the business. Companies that operate in stable, established business sectors, such as most food and beverage companies, are generally advised to adopt riskier incentive plans, such as the fixed number or up-front option grants. They can afford to leverage low business risk with a higher degree of incentive risk. They also need to give their people a strong incentive to strive for continuous improvements in the established processes that are characteristic of mature businesses. By contrast, companies in volatile high-tech or start-up environments, such as many computer or software firms, should moderate their business risk with more conservative option plans, such as the fixed value grant program. As a general rule they cannot run the risk of adding excessive incentive risk to the uncertainties that dominate their businesses.

Management should not rely on these rules of thumb alone to structure their share option plans. A more scientific approach would consider the combined effect of the total compensation package, including the employees’ base pay level, the bonus plan, and the share option program. Management should begin by projecting scenarios for business performance, including best and worst outcomes, and understanding the impact of those outcomes on EProfits and shareholder returns. For each scenario, management should simulate the payments that would arise from the various compensation packages – how much from base pay, and how much from bonus and options, and so on. Companies should evaluate the cost, risk and incentive tradeoffs of the proposed pay strategies.

The companies that have derived the greatest benefit from EProfits have made it a focal point for everything they do. They have used EProfits to establish a common language that has united the often-fractious dialects of individual departments and staff functions. The best companies have also insisted that EProfits be readily available to guide and motivate the behaviour of all their people.

-

Managers in best practices companies have found a variety of techniques particularly effective at making EProfits a core concern. For one thing, they make EProfits the centrepiece of their internal management reporting. EProfits is not just one measure among many measures on their performance scorecard. It is the pinnacle of their reporting pyramid and the value anchor for their scorecards, with all other measures and milestones directly traced to the impact on EProfits.

-

All decisions are EProfits based. Planning, business case analysis, and budgeting have all been reformulated so that it is easy for everyone to project and discount the EProfits that will arise from making business decisions. Top management simply will not accept a project unless it has been justified through an analysis of its EProfits.

-

The bonus that employees will earn from their EProfits performance is updated and reported to them frequently as the year unfolds. Frequent feedback accelerates learning, and stimulates managers to react promptly and energetically to changing market conditions.

-

Reinforce EProfits thinking is to integrate calculations of prospective EProfits bonuses into decision-making tools and templates. Reports are available to simulate how large a bonus the managers will earn if they are successful with proposed new investments or by pursing alternative business strategies, and how much they stand to lose if they are unsuccessful. The managers analyse risk and commit to the strategies more intensely once they are able to study how their own pay will be connected to future performance.

World class companies also take steps to ensure that the mindset of the entire organization is concentrated on EProfits. Training in EProfits is conducted at all levels, including the board of directors. Top management also visibly celebrates successful applications of EProfits. They use internal communications to share interesting case studies highlighting how employees have improved performance and created wealth by putting EProfits thinking into action. Listed companies also used EProfits in their external communications. They announce their adoption of EProfits to their investors, and they recast their presentations to investors prominently to include EProfits.

It typically requires four to seven months for small to medium size companies to adopt EProfits, and nine months to two years for larger and more complex organizations to erect the full EProfits scaffolding, including the incentive program.