What every CEO needs to understand to explain the value gap between the corporate/internal view of value and that provided by the share market.

Every CEO needs to be prepared for the Board’s inevitable question “Why is our share price tracking at its current level?” The answer is often subjective and does not include good quantitative data and logical explanation.

An Investor Diagnostic is meant to demystify the expectations incorporated in the share price and speculated on by the buy and sell side analysts who report on a company. We do this by gathering and analysing data from both external and internal sources. The comparison of these two sources provides a clearer picture to management about where the “perception” and/or the “strategy” gaps exist.

By isolating the nature of any gaps, proactive steps can be taken to close the gap and to communicate with the market and hopefully adjust valuations accordingly.

Introduction

The company producing the best shareholder return is often determined less by absolute performance but rather by its ability as a company to outperform the expectations that the market has placed upon it.

Management often asks “Why is our P/E ratio so much lower than that of other companies?”

While it is possible that the market is undervaluing any given company, the real implication of a low P/E ratio is that the market holds lower expectations for that company’s performance as compared to its peers.

Executives will always have a different point of view - some executives feel their company is fairly valued; and others believe their company is getting the benefit of an a bullish market; whilst others may believe that their company is undervalued.

The more important question is what actions can an executive take to align the market’s evaluation with the company’s strategic plans?

To determine whether a company is correctly valued, management must examine the market’s expectations for its performance and compare them with what management believes it can achieve. Only after this analysis can a company determine whether a valuation is sustainable. A large part of this analysis involves analysing what the market believes.

Once management understand expectations then these must be incorporated in setting company strategic goals, since generating shareholder returns means exceeding market expectations.

The information, which listed companies, provide to investors, equity analysts and others is a key determinant of market expectations however, analysts also refer to other information when developing their forecasts. This information includes the credibility of management, competitive data, expectations for market demand, etc., which we call non-financial measures. The result is that analyst expectations can and do vary significantly from those of management.

Given the role that market expectations play in determining shareholder returns, the first step in the process is for management to gauge the extent to which internal forecasts differ from external expectations. Only then will it be able to determine whether achieving its current targets will translate into superior shareholder returns.

Measuring Market Expectations

There are three steps involved in gauging market expectations:

-

Performing an investor diagnostic

-

Estimating value creation implications

-

Determining implications for management

Performing Investor Diagnostic

The most obvious way to understand market expectations is to ask equity analysts, whose job it is to inform investors, and when feasible, buy-side analysts, whose job it is to make investment decisions. These surveys are designed to uncover the following types of information:

-

Consensus forecasts for revenue, profits and free cash flow for the total business and key business segments/units

-

Quality and quantity of information provided by management to investors

-

Investor’s perception of management and management’s ability to consistently meet its public commitments

-

Performance indicators which analysts consider most important

-

The extent to which analysts feel the total business and the most important units are fairly valued by the market

-

The extent to which analysts understand and accept the total business or unit’s business strategy and/or key strategic initiatives

-

The strategic fit among the company’s portfolio of businesses

The objective of the interviews is to identify and to understand the key factors driving analyst’s expectations for a company’s performance. Many times these objective third party discussions reveal the bias of selected analysts as they weigh specific factors. They also ascertain the investment community’s attitudes on qualitative perspectives that are generally not discussed during analyst meetings. The benefits. of these interviews, are that they can isolate and clarify specific issues that may be affecting how a company’s message is being received.

Estimating Value Creation Implications

The next step involves translating analyst’s expectations into a consensus view of the value they expect the business to create overtime. Understanding the value of existing operations, plus the value of future growth options does this.

The baseline value in this calculation is defined as the value of a business with zero anticipated value creation – that is, the value of the companies existing operations. Therefore, by subtracting baseline value from the total discounted cash flow business value, we can isolate the expected value creation or the value of the future growth options.

The advantage of measuring value creation expectations of analysts is that it provides a true economic “bottom line” for which to compare value creation anticipated by management’s strategic plans. Without this “bottom line” it would be difficult to compare an analyst forecast with high cash flow to a management forecast with lower earnings but also much lower investment requirements. This measure of value creation can determine which of these two forecasts generates the most value for shareholders and can be used to further illustrate the strategic thought process that the company used to develop its forecasts.

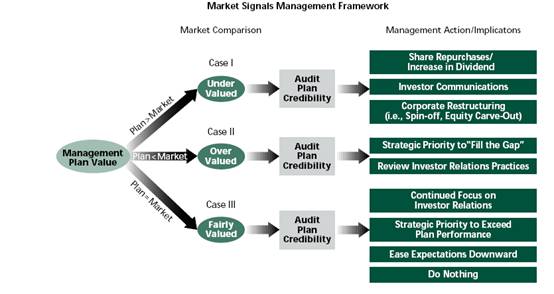

Armed with management and market expectations of value creation, there are three possible scenarios that can be considered. The three possible outcomes of comparing internal and external expectations imply very different management actions.

The Company could be Overvalued

If a conclusion is that the shares are overvalued, then management has several potential remedies. Firstly, the business strategy should be re-examined to determine if there are any ways to close this “strategy gap” and to generate the level of performance required to support the current stock price. Examples of ways to create value in line with expectations include:

-

Performing synergistic acquisitions especially deals using high-priced stock as currency

-

Entering new geographic markets

-

Pruning value-destroying business and activities

-

Re-examining the firm’s marketing and distribution practices

-

Selling the business to a synergistic buyer at a hefty premium

If none of these approaches are feasible, management’s second option is to communicate to investors that the market is being too aggressive and the company cannot deliver the performance required to justify the current stock price. If management can find no way to justify or deliver high market expectations, it is usually advisable to communicate this to the market rather than remain silent. Doing so strengthens management credibility, which is a critical ingredient in managing investor expectations over the long-term.

How do market expectations exceed management’s plan? Maybe its because of management track record of conservative forecasts. Alternately the market may not be anticipating major investments required in certain businesses in order to support growth. The result is that management has to deliver more the value creation anticipated in its plan just to meet market expectations.

The Company could be Undervalued

There are two potential reasons that the market may appreciably undervalue the company. First, management’s plan may be considered unjustifiably aggressive in the eyes of the analysts. This may be a “perception gap” and management should examine its track record for delivering against prior forecasts. If a company finds itself consistently below plan, it should critically evaluate its long-term strategy to determine if expected operating performance levels are truly achievable.

If management is satisfied that the strategic plan is credible, then a second possible reason for the undervaluation is that the market has not given this plan fair credit. This “perception gap” could exist because analysts lack necessary information; for example, management may be reluctant to divulge certain information necessary to render a fair judgment for competitive reasons. Often companies have developing businesses, which are not included in management’s plan. Analysts are unable to value these and therefore give them no value primarily because management had not divulged any information about their prospects

There are several possible actions:

-

First, the investor relation’s strategy can be altered to improve the quantity and quality of information provided to the market

-

Alternatively, a share buy back can strongly express management’s belief that its’ shares are undervalued without revealing competitively sensitive information. Personal purchases by senior management are another very positive signal

-

Management may suspect that a particular business unit may be the source of the undervaluation. This can be true of high growth businesses embedded in low growth parent companies. In this case, companies should consider selling a portion of the division with bright prospects to the public market. In doing so, the market often receives more information about the unit and is forced to render a judgment regarding its value

Alternately the Company could be Fairly Valued

In the event that market expectations closely mirror management’s plan, the implications are not altogether dramatic, but the prospects for value creation are similarly not altogether exciting. Basically, everyone is in agreement. If management achieves its goal, then shareholders can expect to earn only their required return and no more. Therefore, management’s focus should be to examine opportunities to exceed its plan. Similarly, performance targets and incentives might be structured to ensure that the plan represents a minimum level of performance.

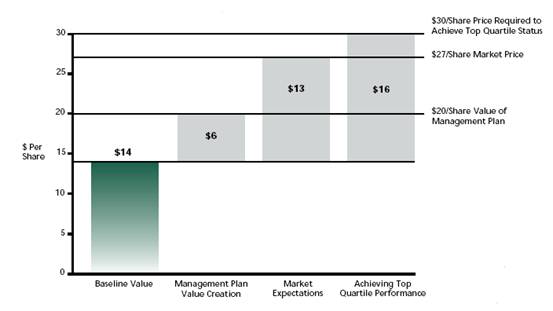

Conclusion

In order for managers to be confident that they are creating value, they must examine the expectations held by the market and find ways to continually exceed them. In carrying out the value gap analysis it is helpful to determine four components of value, as outlined in the following diagram: the baseline value (current value of operations), managements value creation strategy (their growth options), market expectations (implied market growth options) and what value is needed to be achieving top quartile performance. In addition its critical to understand the impact of non financial measures on the valuation outcomes since our studies have concluded they can account for some 40% of the market value of a company.